This post will provide a graphical update on what has been a roller coaster ride in the natural gas market over the past 12 months, and a steep plummet of late. Natural gas prices have dropped by 50% in the last month, and over 70% from their highs earlier in the year. The warmest winter on record and not a single rig-damaging hurricane have combined to create record gas in storage, thereby reducing price demand for the marginal unit. Yet, production is flat with last year despite significant more drilling and rigs allocated to the commodity. The current situation is thus one of short term plenty and long term supply concern. If longer term predictions of reduced supply and accelerated well depletion are correct, we should be seeing some of the major producers reduce rig counts at these levels, or shut-in their production with intent to sell it higher in the future. This post examines the supply/demand equation for natural gas in the US, the NG futures strip, and the implications going forward of higher price volatility in this important commodity.

[break]

(For those unfamiliar with how the energy futures markets work, here is some background info.)

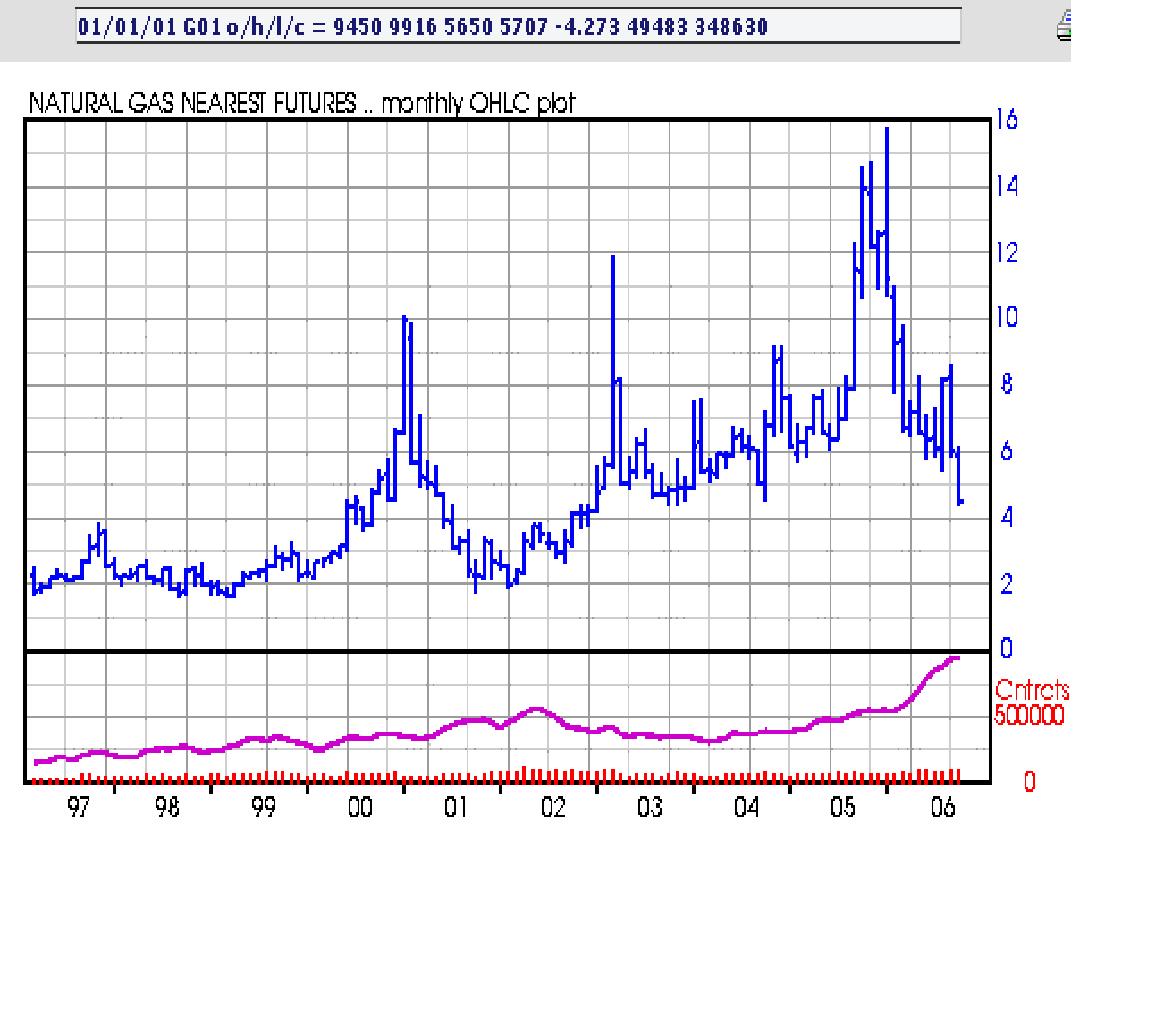

Natural gas. It does everything from heat our homes to fertilize and cook our food. And unless you've lived in a climate that doesn't require air conditioning or heat, you've probably heard of the wild swings in the gas market in the past year. The price drop has caused fits, threats and lost bets. Each day the natural gas market goes up or down. This year, its pretty much gone down.

Click to enlarge.

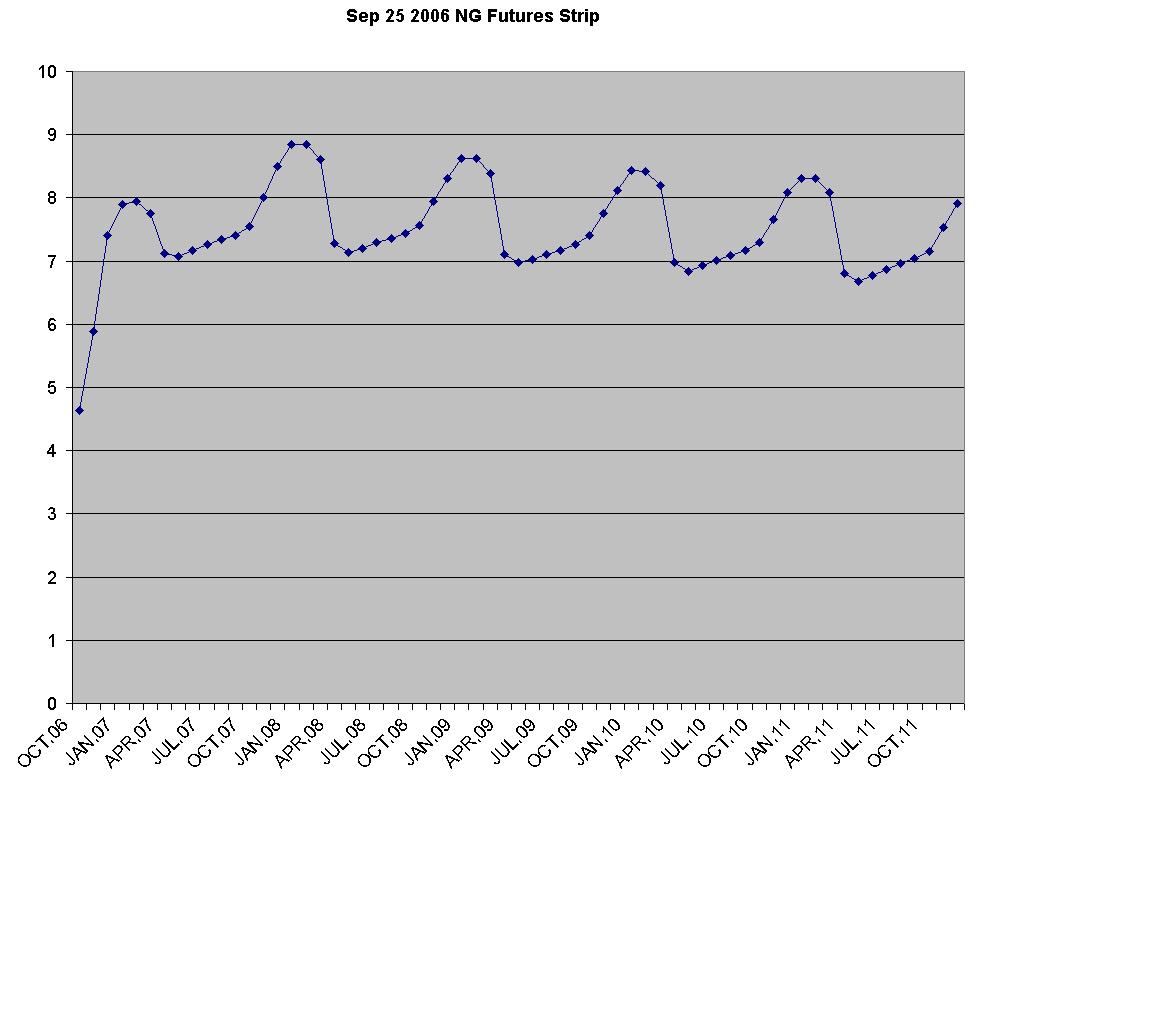

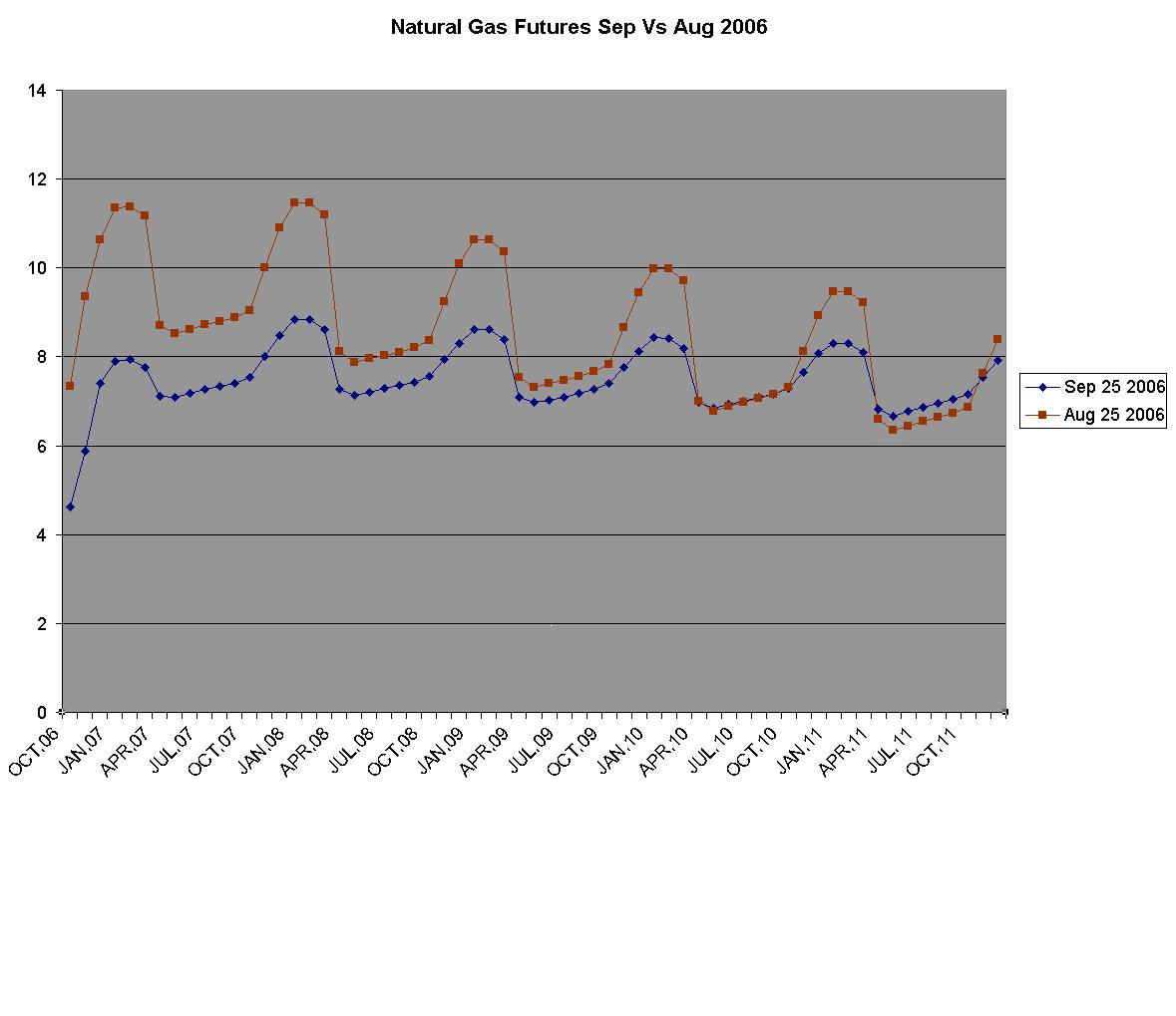

The two markets I refer to in the title are supply and demand. But I could just as easily be referring to the dichotomy between near term prices and long term. The above chart (and most news services (CNBC, etc) quote what the 'front' or near month for oil and gas futures is doing. However, these commodities can be traded for expiration each of the next 60 months. A 'futures strip' is comprised of the entire forward market for a commodity. The complexity of the short and long term supply/demand situation can be better understood by looking at the entire curve. Below is a graphic of the futures strip from NYMEX.com of last fridays close for natural gas. (it was down again on Monday). As can be seen, prices are very low for October and November 2006 then form a sine wave pattern for the next 60 months, with peak prices expected in winter months, when heating demand is high. (Note, the above chart shows historical prices over 10 years, the below chart are todays prices for delivery the next 5 years in the future)

Click to enlarge.

We will return to the futures strip at the end of this post but first give a review of the current dynamics of the natural gas market.

NATURAL GAS SUPPLY

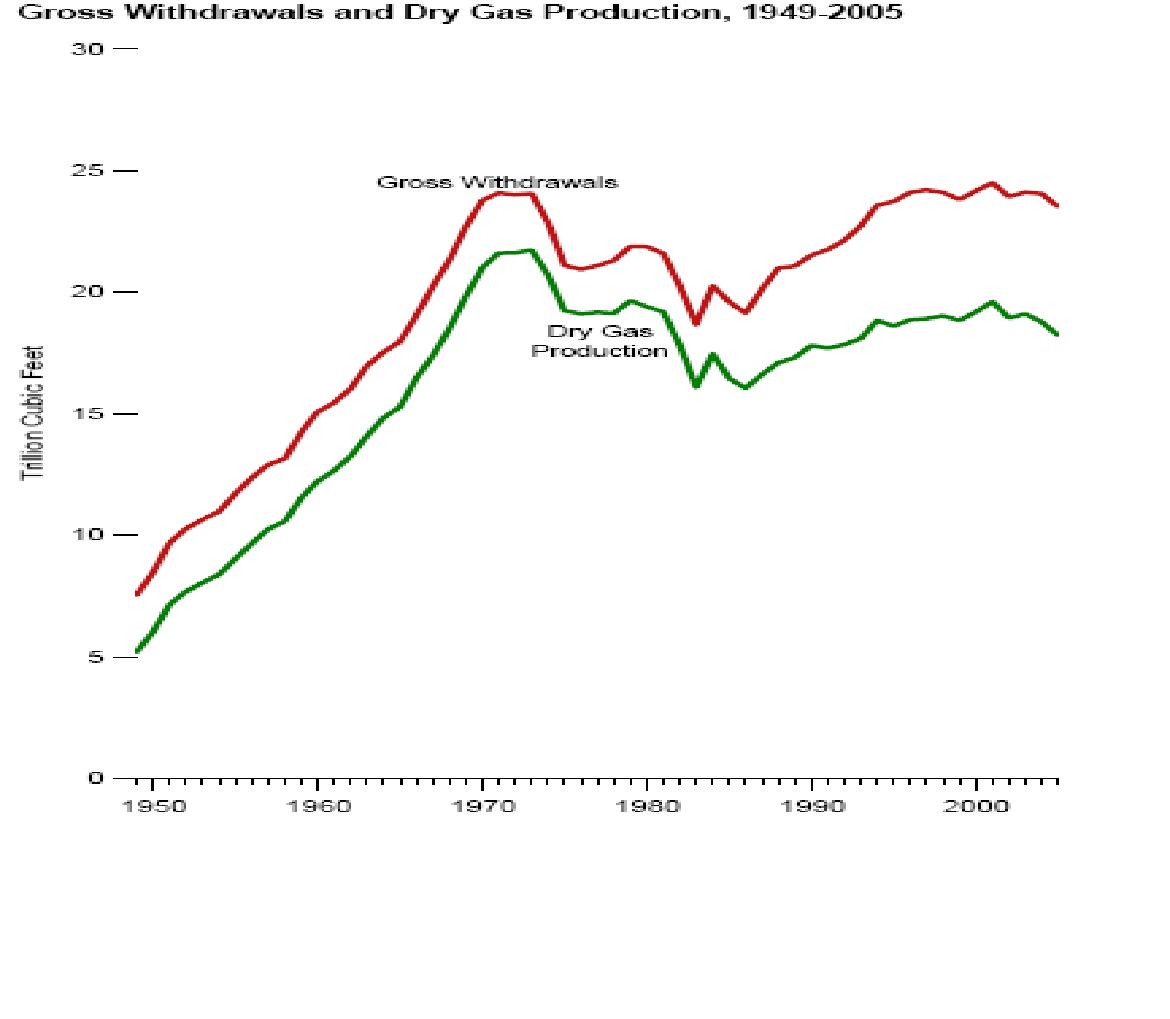

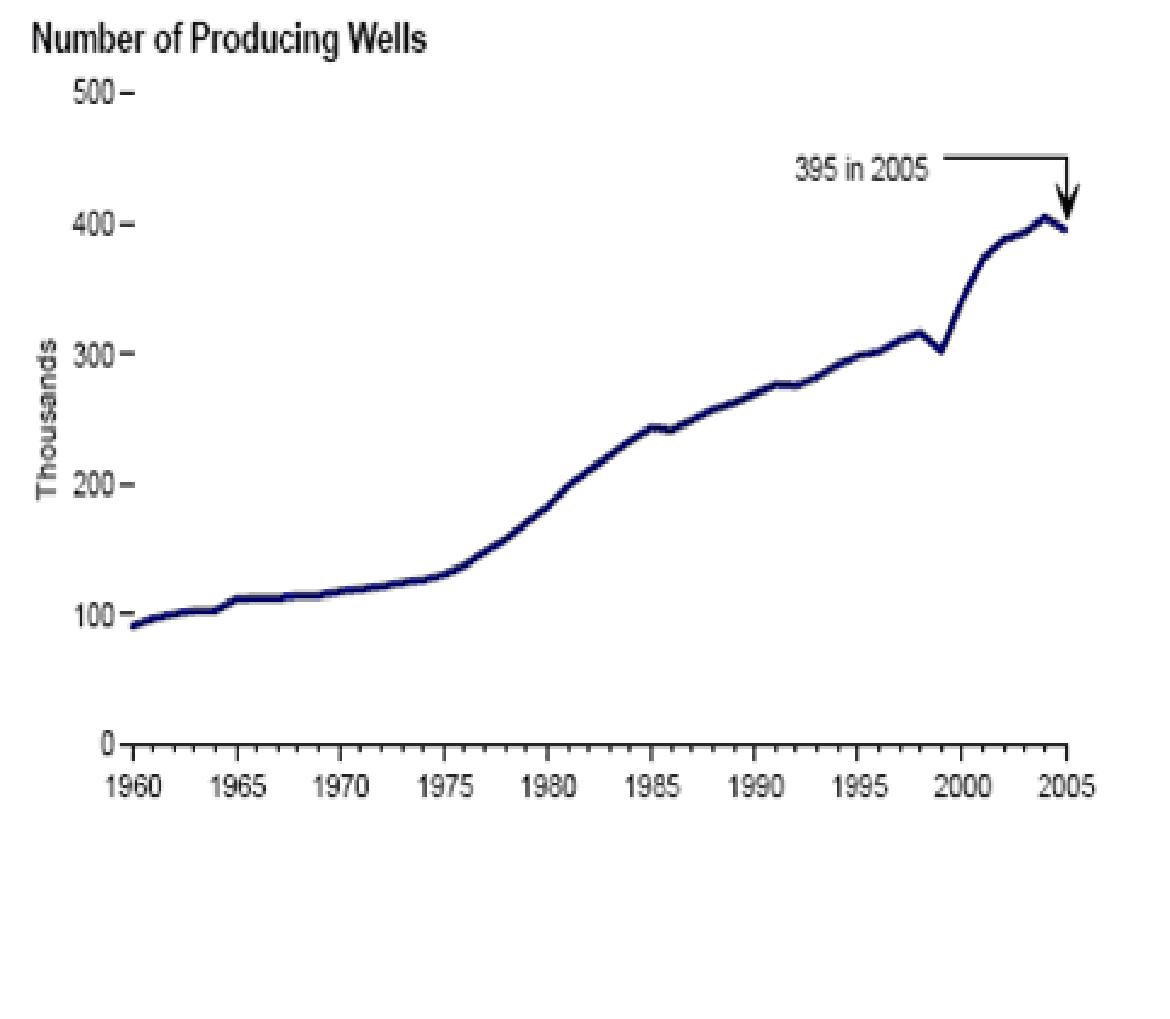

The Peak Oil (and Natural Gas) crowd typically focus their worries on the supply side of the market equation. The supply story for natural gas, at least domestically, does not look promising. The United States has roughly 400,000 natural gas wells operating currently, near an all time high. First of all, lets look at total production in the United States. (The difference in the two lines is the top one includes 'wet gas' or non-gas liquids which are added into the petroleum supplies.) (Source EIA)

Click to enlarge.

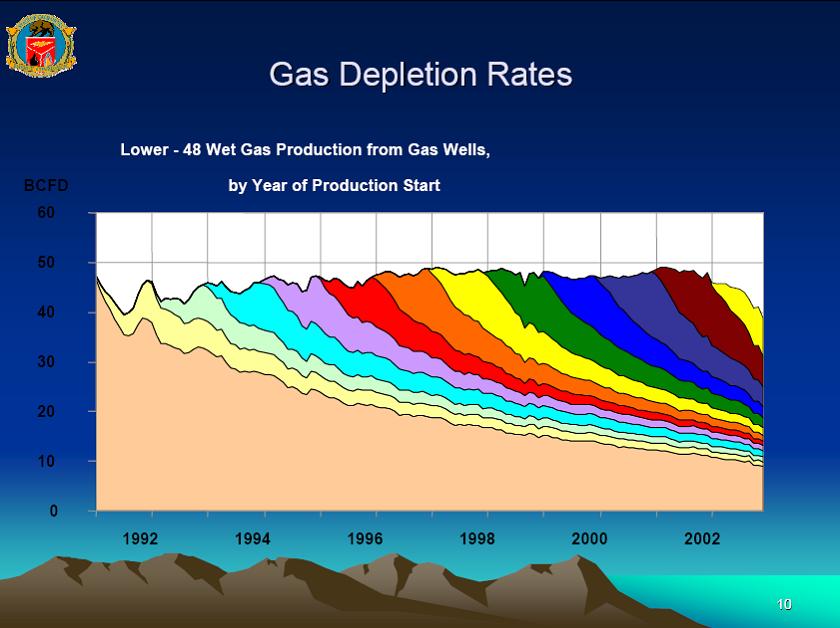

The following is a graphic showing how quickly the average new gas well is depleted. (this is for wet wells but dry wells appear to be depleting slightly faster) As can be seen, a decade ago, it took 10-15 years for a new well to deplete. Now they are going dry in less than 18 months.

Click to enlarge.

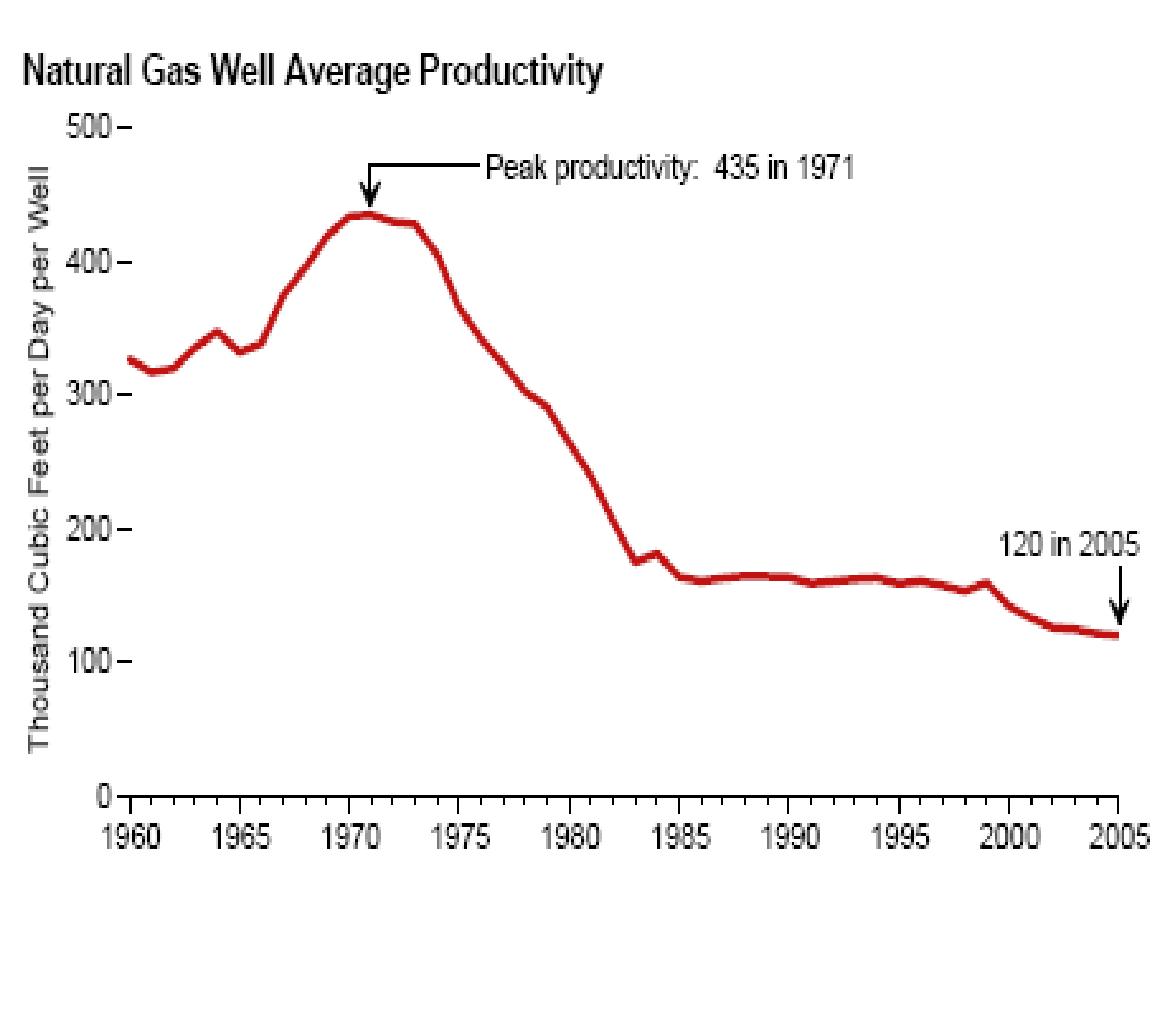

In addition to quicker depletion, wells are smaller and hence less productive: (Source EIA)

Click to enlarge.

We are drilling more wells and smaller wells. Equity research house Johnson Rice recently put out a report showing that from Q2 2005 to Q2 2006, the top 20 NG production firms were down 2.4% in production yet had increased rig count by 22%. (this doesnt include shut-in production).

HELP FROM THE NORTH?

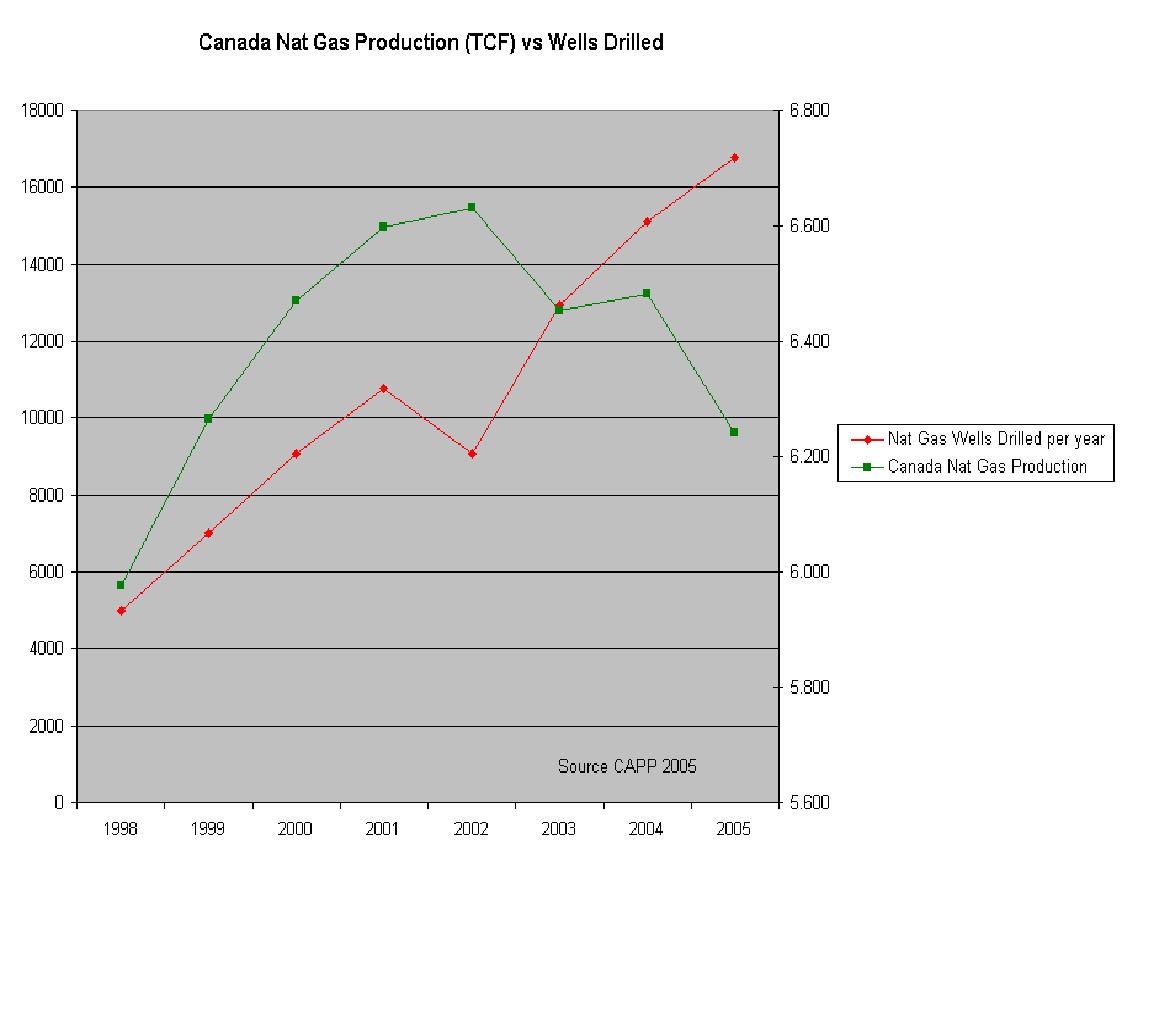

Canada produces about 6.2 TCF per year and exports 3.6 TCF to the United States. However, they too are declining in production with a large increase in wells - a similar pattern to the US. The graph below shows Canada producing about the same amount of NG as in 1998, but needing to drill more than twice the wells annually to do this. (Don't get me started on net energy)

Click to enlarge.

This is a broad sketch of the supply picture - of course there are coal bed methane and liquefied natural gas, but the impact of both is uncertain, and with natural gas currently with a $4 handle, those sources may be uneconomical or not come to market in a timely fashion. To me, the North American natural gas supply situation can best be likened to the Red Queen in Alice in Wonderland, who kept running very fast just to stay in place - if she slowed down, she might go backwards rapidly.

NOT SO FAST MY FRIEND!

Natural gas demand is the other half of the story. The US (in 2005) used just under 22 trillion cubic feet of natural gas. Believe it or not, this is less than we used 10 years ago (compared to a 13% increase in crude oil).

The 22 TCF roughly breaks down as follows: 24% for residential heating, 14% for commercial use, 35% for industrial use, and 27% for electric and combined cycle power.

Click to enlarge.

Though many say that closure of industrial and chemical plants domestically due to high NG prices is responsible for the drop in industrial demand, as can be seen from the chart, this trend has been in place since the late 1990s, when gas was still cheap. If I was a manufacturer in Toledo paying $17/hr why wouldnt I move my plant to Mexico and pay $4/hr for wages? It is unclear how much more demand destruction can come from the manufacturing sector. However, electricity demand and its use of natural gas has surely been growing.

THE NEW GODZILLA MOVIE - "GLOBAL WARMING VS GAS DEPLETION"

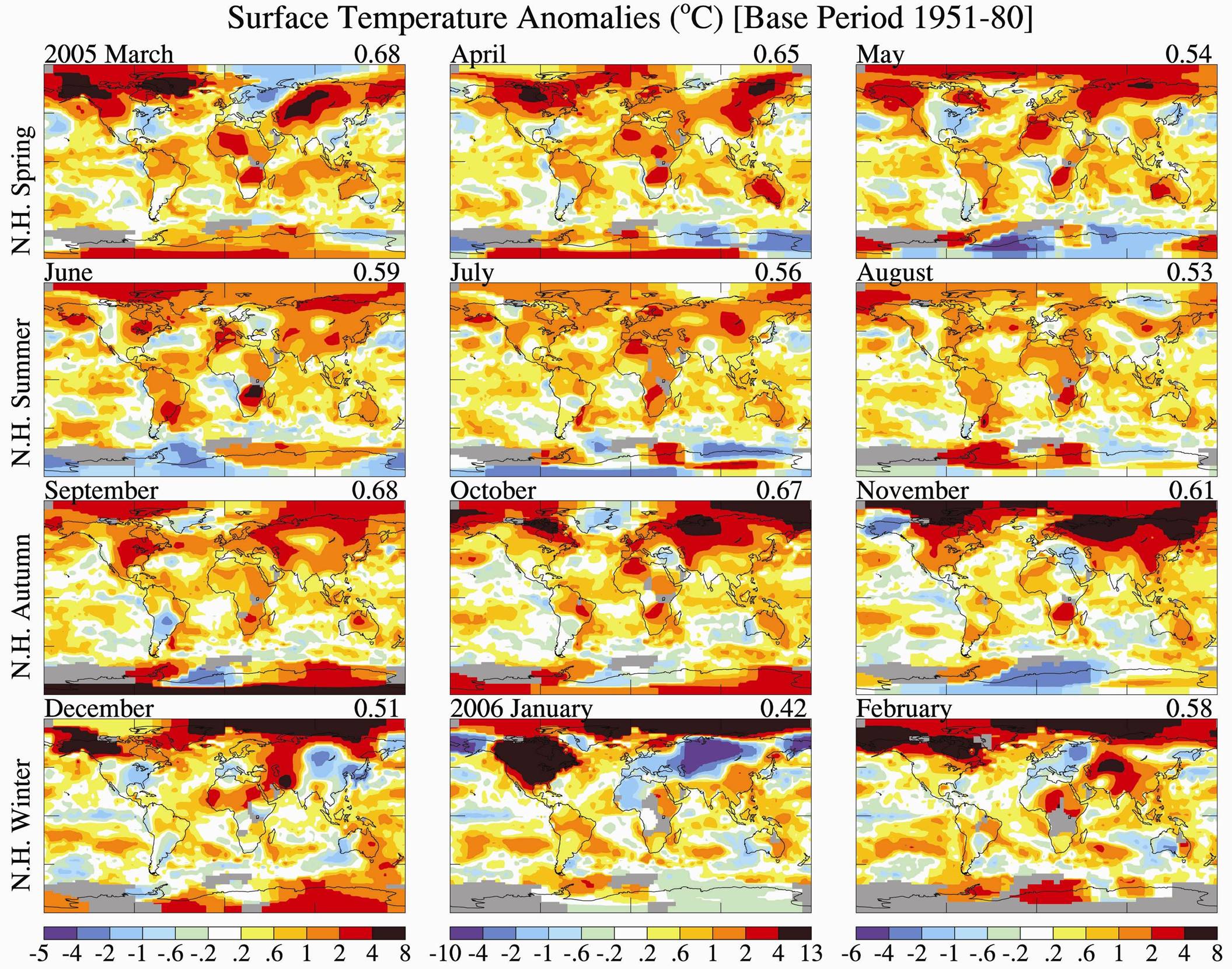

The past winter was the warmest on record. But just how warm is not commonly known. The dark red patches in North America in the below graph are 4-13 Degrees C above the historical average - needless to say, less people needed natural gas for heat (except in Russia - where they had the opposite trend in January)

Click to enlarge.

(Source - James Hansen NASA 2006)

The warm temperatures contributed to much less demand for heating not only in the dead of winter, but in the spring as well. April, May and Jun 2006 each saw less natural gas usage than any equivalent month for the last 33 years. So far through 2 quarters in 2006, residential customers have used 12% less natural gas than 2005.

BACK TO THE FUTURE(S) - WHAT A DIFFERENCE A YEAR MAKES

Click to enlarge.

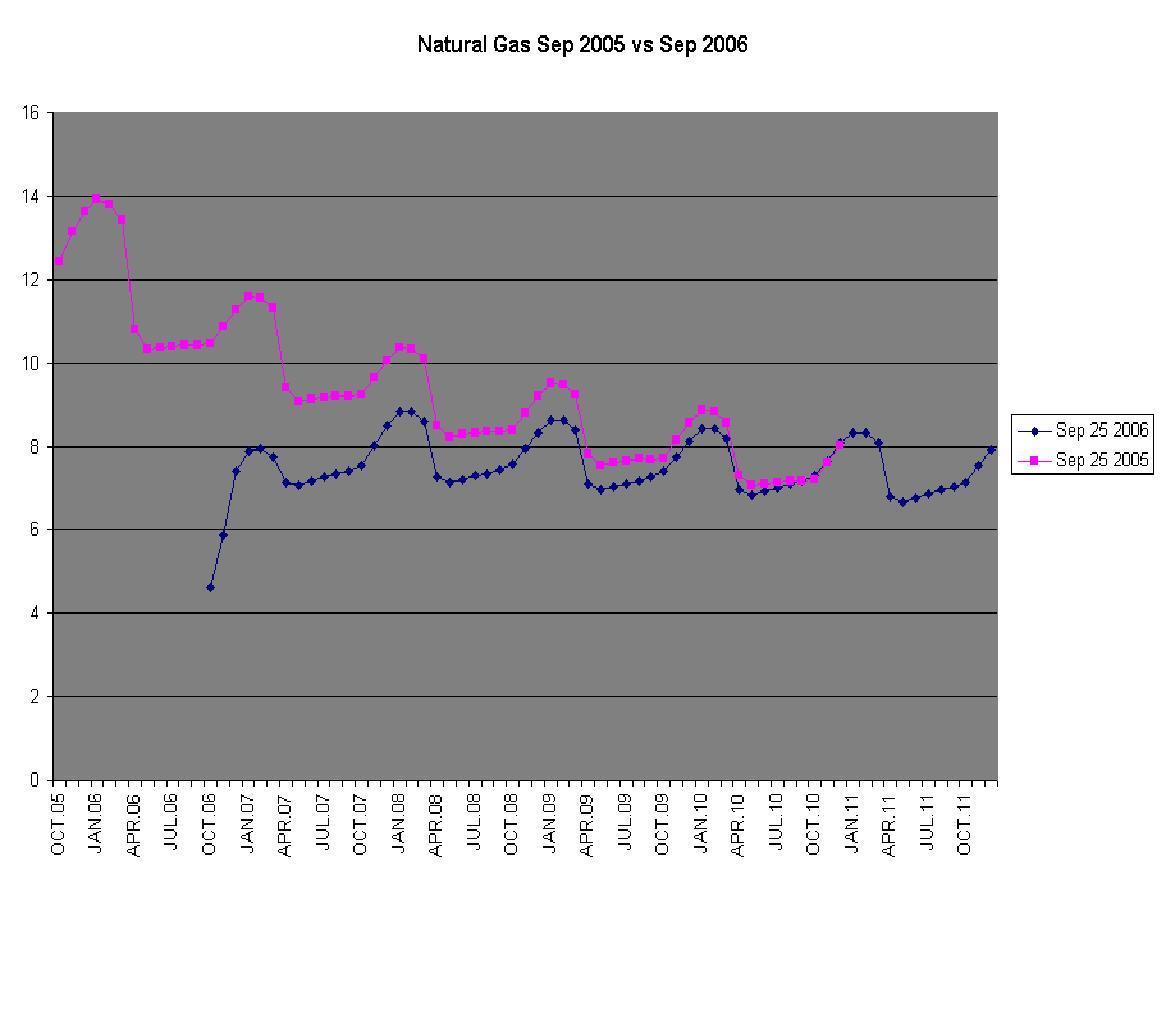

The pink line represents what the futures strip looked like in September 2005. The blue line represents the futures strip on Friday. (Notice, we are missing 12 months of pink line at the end because last year 60 months only brought us to 2010 and we are missing 12 months of blue line at the front because fridays futures are only looking forward, not backward)

What we see here is that the front month, which at one time was over $15 is now at around $4.50, an historic drop. However, a year or so out there has been a much smaller drop and at the end of the futures strip (2011) prices are actually slightly higher than they were a year ago. We also can see that winter months command higher prices, due to higher chances of shortages when natural gas usage is highest. Also, the shape of the winter 'hump', though at lower levels, is similar to a year ago. We also notice that currently all winters in the future are roughly priced the same, whereas a year ago, the nearer the winter, the higher the price.

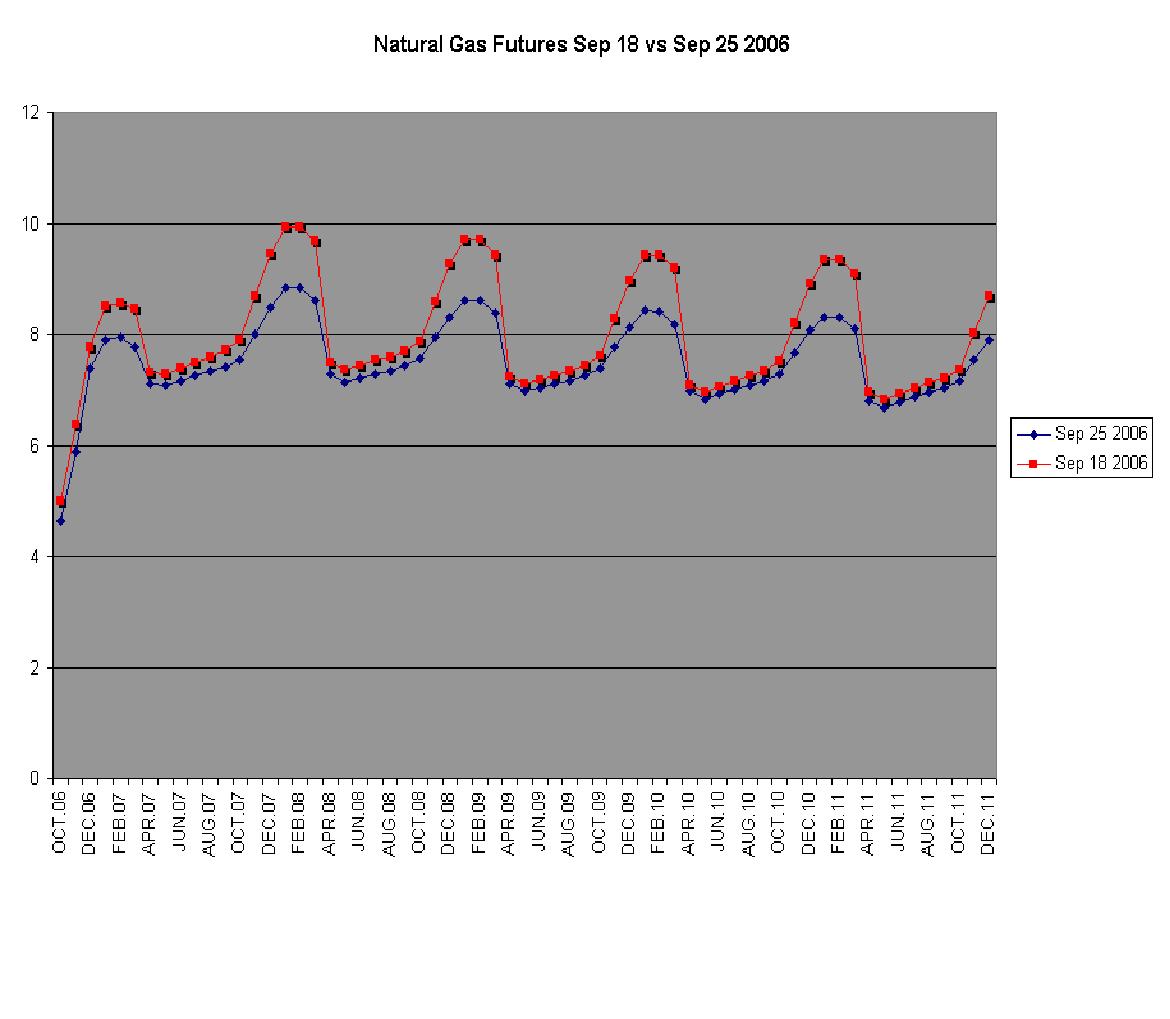

WHAT A DIFFERENCE A MONTH MAKES

Click to enlarge.

What does this graph tell us? First of all, near month futures have dropped like a stone since August - from near $8 to $4.50ish. Also, the winter-summer premium has declined, not only in this coming winter (where supposedly Amaranth had their calendar spreads), but in all subsequent winters. Either there was some major hedge fund activity, or some energy traders talked to Al Gore. Curiously, in the face of this steep decline, back dated futures actually went up (the blue is higher than the brown in 2011)

WHAT A DIFFERENCE A WEEK MAKES

Click to enlarge.

Here we can see that in all years except for 2006, the majority of the winter-summer premium collapse of the last month came in the last week. (compare the brown-blue vs red-blue in the two graphs). However, this winters price differential had already collapsed, presumably earlier in the month, from about a $2.50 premium over spring to about $1.

If we believe the media reports of Amaranth losing $6 billion, how could they do that in natural gas calendar spreads? First of all, each natural gas futures contract is 10,000 million BTUs or 10 million cubic feet of gas - this means for each 1 point movement in price, the contract value changes by $10,000. So to lose $6B, one would have to have on 400,000 contracts if there was a $1.50 loss. However, the entire open interest of all the 2006-7 winter months is about 260,000 contracts and the entire open interest of every contract thru 2011 is 960,000 contracts. So either Amaranth had off balance sheet exposure (derivatives), they had things other than calendar spreads on (the actual front month contract declined almost $4), or something else was afoot.

Incidentally, if they did have 400,000 contracts, that would represent 4 trillion cubic feet, or about 20% of US annual natural gas consumption. Boy do energy and dollars make strange bedfellows...

AND FOR SOME PERSPECTIVE

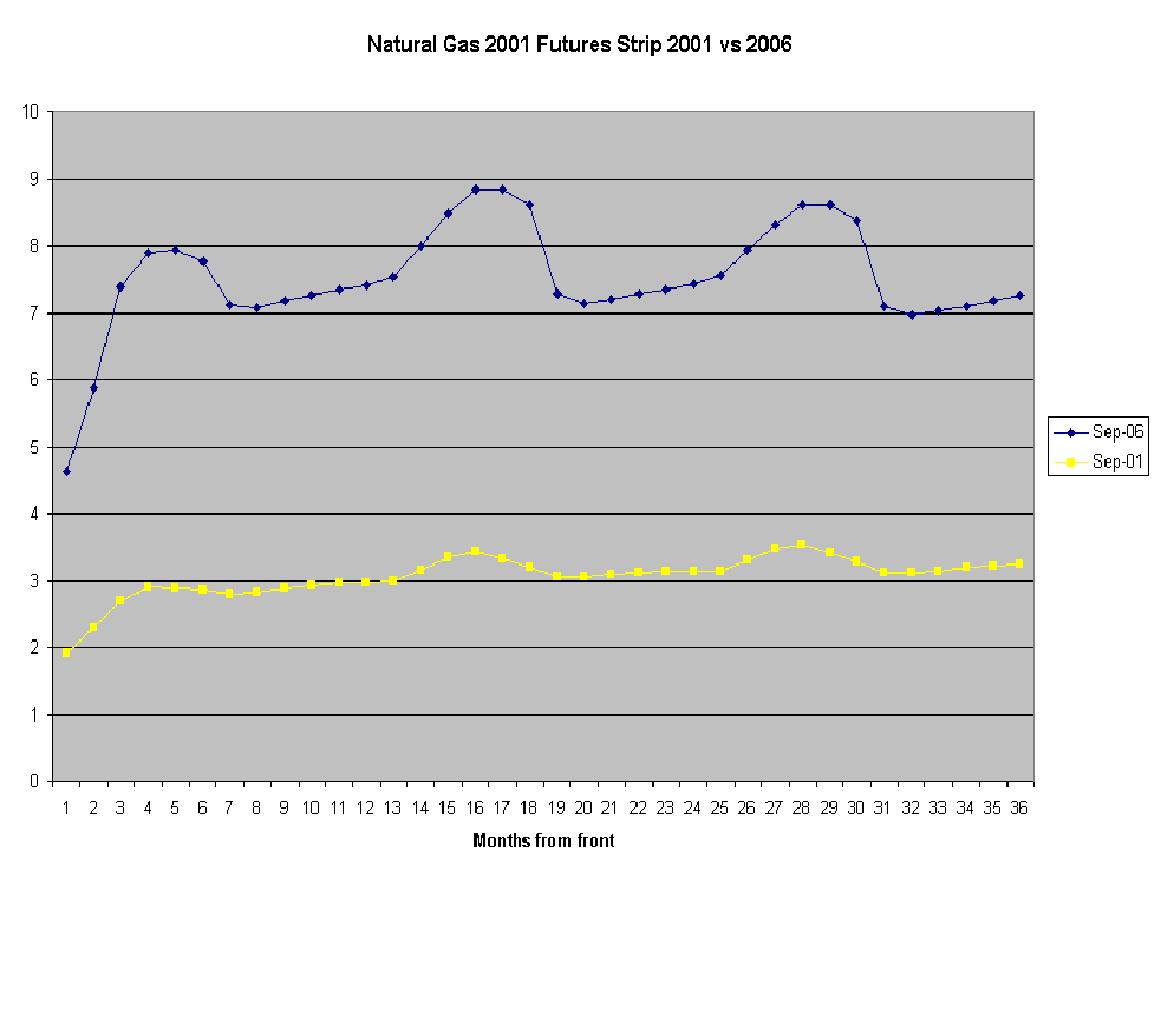

Keep in mind that despite the dramatic fall in natural gas prices in the past year, when we compare the current futures strip to what it looked like 5 years ago, we see a) current prices are still much higher that they used to be and b) the winter 'humps', though still existent 5 years ago, were much smaller.

Click to enlarge.

{kind=link}

{kind=link}

{kind=link}

CONCLUSIONS

We currently have a glut of natural gas. As scary as the future supply situation is, the fact is that even with a cold winter supplies will be adequate. Could another warm winter (it is an el Nino year) combined with no increase in storage capacity result in actual flaring of gas? Producers wouldn't allow this to happen of course, as at SOME price they will shut-in production and stop drilling new wells. In fact, today Baker Hughes announced their new weekly rig count, and the Canadians, always quick to reduce drilling on commodity price drops, had a 22% drop in rigs from last week. High prices gave us demand destruction. Low prices give us supply destruction.

Low prices, while currently pleasant, send the wrong long term signal to the alternative energy markets (like wind, tidal, solar, etc). Energy price volatility (in both directions) interrupts progress being made replacing fossil fuels with renewables. Low natural gas prices remove the motivation of utility providers to invest in alternatives. Low prices also prevent wind and solar entrepreneurs from being cost competitive, until the signal is too late. Furthermore, continued volatility will hamstring policymakers. A warm winter and everything is fine and a cold winter and people freeze in Michigan. As James Schlesinger, our nations first energy secretary said about energy "We have only two modes--complacency and panic." I can think of a third mode -schizophrenia due to alternating years of complacency and panic.

Towards this end, and this applies to crude oil as well, the ease with which the wall street crowd can impact the price of a commodity that is so ubiquitous in making our system work, combined with growing knowledge that fossil fuels are a one time subsidy given to humanity and are depleting rapidly, should alert policymakers to the importance of making immediate changes to current energy policy. In addition to position limits for non-users or hedgers of energy, we should create a floor price for oil and gas, so that financial market-led volatility or intermittent gluts of product do not derail the development of alternative forms of electricity and liquid fuels. The achilles heel of the big two fossil fuels in their use in our world, is the time it takes to replace them. The natural gas market, in its current price dichotomy, is a prime example of the high standard deviation potential in our current system. Heads everything is rosy. Tails there are power outages.

I have no idea whether it will be cold this winter.

*Note - Thanks to Art Smith of John S Herold and Co., Joann Arena at the New York Mercantile Exchange, Neal Elliot at ACEEE, and John Rowan at Johnson Rice for data that was used in this post.

No comments:

Post a Comment